Running a small business in South Africa brings unique financial challenges: from delayed payments to load-shedding disruptions. Two financial concepts—liquidity and cash flow—can make or break your operation. Knowing the difference and actively managing them is vital for your business to survive and thrive.

This guide breaks these concepts down clearly, explores how to measure and improve them, and shows how ProInvoice can be your most powerful tool in making both work in your favor.

1. Defining Liquidity: Your Readiness to Pay

Liquidity refers to how easily a business can meet its short-term financial obligations using available assets. It isn’t only about the cash already in the bank but also other assets that can quickly be converted into cash—like receivables or short-term investments.

In South Africa’s unpredictable economic environment, good liquidity ensures you can pay employees, suppliers, or unexpected costs—even during hard times like power outages or market shifts.

2. Understanding Cash Flow: The Rhythm of Your Business

Cash flow tracks the actual movement of money—both incoming and outgoing—over a set period.

Think of liquidity as your business’s “cash on hand to cope,” while cash flow is the heartbeat—how money flows in and out. In South Africa, poor cash flow management is a top reason for business failure, making accurate cash flow projection critical.

3. Liquidity vs Cash Flow: Related But Distinct

While intertwined, liquidity and cash flow tell different stories:

- Liquidity measures immediate financial safety—do you have enough accessible assets to meet obligations?

- Cash flow shows whether your business is generating enough income over time to be sustainable.

A business might be profitable on paper but still run into trouble if cash doesn’t come in quickly enough—or if assets are tied up.

4. Measuring Liquidity: Key Financial Ratios

Liquidity can be assessed using several ratios:

- Current Ratio = Current Assets / Current Liabilities

- Quick Ratio (Acid Test) = (Cash + Receivables) / Current Liabilities.

These reveal how well your business can cover short-term debts without harmful asset liquidation. In volatile South African markets, maintaining a buffer above 1 is often recommended.

5. The Importance of Cash Flow Forecasting

A cash flow projection helps you predict future liquidity scenarios—anticipating cash shortages or surpluses.

By forecasting monthly inflows (sales, loans, investments) and outflows (rent, salaries, suppliers), you can manage risks—such as load-shedding costs or client payment delays.

6. South African SMEs: Unique Liquidity Challenges

Local businesses face challenges like delayed B2B payments, impaired access to capital, and operational disruptions.

Building cash reserves, negotiating better supplier terms, and automating receivables are critical strategies to mitigate risk.

7. Liquidity Management: The Strategic Approach

Liquidity management means balancing inflows vs. obligations—ensuring sufficient, strategic cash use for optimal operations.

A strong liquidity plan helps you sustain operations, invest smartly, and adapt to disruptions—all while avoiding excess idle cash.

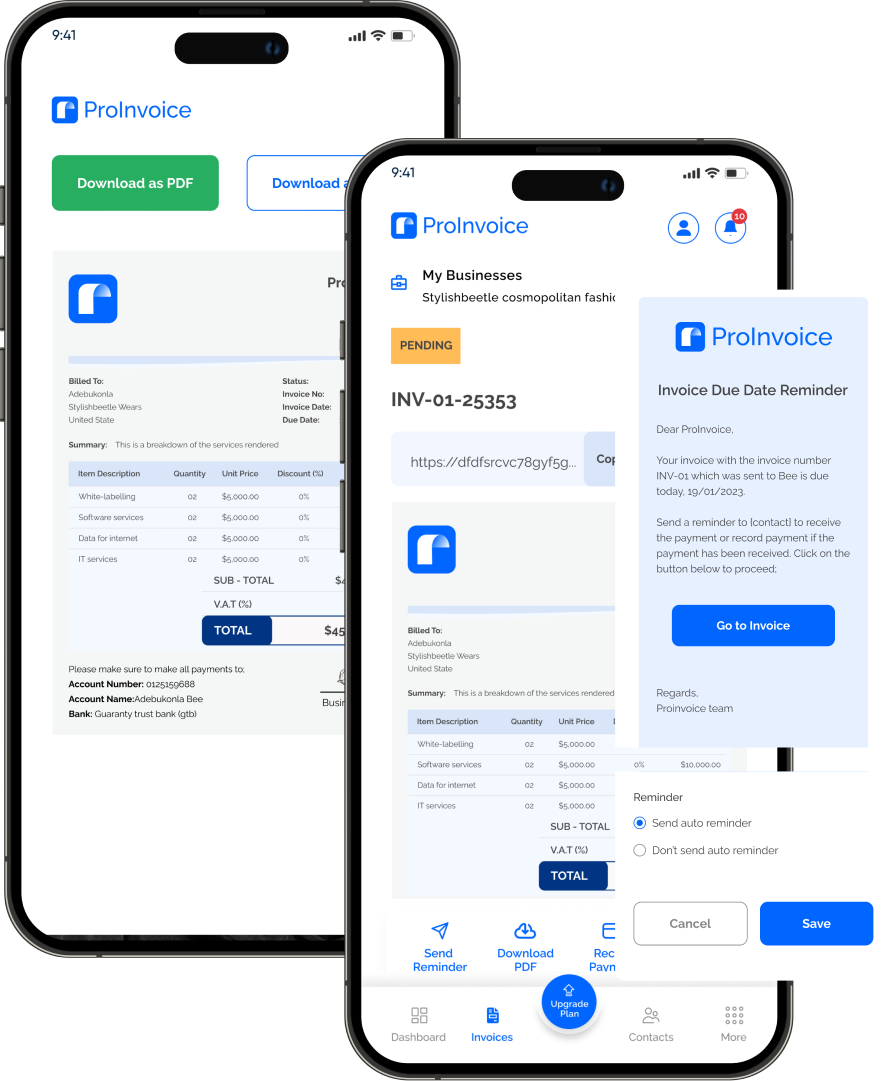

8. How ProInvoice Supports Cash Flow & Liquidity

Cash flow and liquidity are only manageable with accurate invoicing and payment tracking—and that’s where ProInvoice shines:

- Generate and send invoices instantly—ensuring faster client payments.

- Track receivables; send automated reminders for overdue invoices.

- Export transaction histories to monitor inflows vs. liabilities.

- Use real-time visibility to inform liquidity planning.

By improving invoice turnaround, ProInvoice directly improves your cash flow and, ultimately, your liquidity.

9. Tips to Improve Both Liquidity and Cash Flow

a) Invoice Promptly and Accurately

Delays in sending invoices delay your money. Tools like ProInvoice speed up delivery and tracking.

b) Offer Early Payment Incentives

Provide a small discount for payments received within 7–10 days to boost liquidity.

c) Build Cash Reserves

Automatically set aside a portion of monthly revenue into a separate savings buffer—for disruptions or opportunities.

d) Negotiate with Suppliers

Longer payment terms reduce immediate pressure on cash while you manage receivables.

e) Monitor with Metrics

Use the current ratio, quick ratio, and cash flow projections to regularly assess risk and readiness.

Final Thoughts

For South African businesses, maintaining good liquidity and strong cash flow isn’t optional—it’s essential. Each supports continuity, growth, and resilience against economic or operational shocks.

And with ProInvoice powering your invoicing and receivables tracking, you gain real-time insight and control—turning healthy cash flow into reliable liquidity and a secure foundation for growth.

Ready to take control? Sign up for ProInvoice free today and start managing your cash smarter.