Access to affordable financing remains one of the biggest hurdles for Nigerian entrepreneurs. Whether you’re building a small-scale agribusiness, tech startup, retail store, or consulting brand, you’ll likely need capital at some point.

In 2025, businesses now have more access to formal and informal loan options—but the application process still feels overwhelming.

This guide covers how to prepare, apply for, and manage a business loan in Nigeria step by step. Plus, as you grow, tools like ProInvoice help you issue professional invoices, track your cash flows, and demonstrate credibility to lenders and clients.

Let’s get into it.

1. Understand Your Funding Needs

Before you apply for a business loan, ask yourself:

- How much do I actually need?

- What will the money be used for?

- When do I expect to pay back?

- How will this loan increase revenue?

Create a simple financial plan or projection—even in a spreadsheet—to show lenders your repayment strategy.

2. Know the Types of Business Loans Available

a. Bank Loans

Offered by commercial banks for businesses; require collateral and sometimes group guarantors.

b. Microfinance Institutions (MFIs)

Smaller loans (₦50k–₦2M) with lower interest rates and flexible repayment periods.

c. Government & Development Fund Schemes

Includes programs like NIRSAL, YouWin, CBN agro-loans, AVANCE, and state SMEs.

d. Digital Loan Apps & FinTech Platforms

Apps like FairMoney, Branch, PalmPay, and others offer quick, small cash advances without collateral.

e. Credit Unions & Cooperative Societies

Local groups pooling funds to lend to members at favorable terms.

3. Get Your Business Documents and Financials Ready

To qualify, you’ll need:

- A registered business name or CAC certificate

- A bank statement (ideally 6 months of activity)

- A brief business plan or use of funds explanation

- Proof of revenue history if available

- Collateral documents, if required (land, shop lease, equipment)

If you’re just starting, you may use projected sales, a clear repayment plan, and a savings or investment history (e.g., PiggyVest or Cowrywise).

4. Choose the Right Loan Option for Your Business

Match your situation with the most realistic option:

- Need ₦100k–₦500k? Microfinance or fintech apps are ideal.

- Need ₦1–5M? Consider SME-focused banks or your existing account.

- Need ₦10M+? Approach commercial banks, government scheme offices, or investment portfolios.

Always read the terms carefully—interest rate (APR), repayment period, and hidden fees vary by lender.

5. Apply the Right Way: Steps to Follow

- Visit lender’s website or branch to request application forms.

- Fill out application clearly, including your business purpose and repayment plan.

- Submit required documents—CAC, bank statement, ID, business proposal.

- Provide collateral or guarantor, if needed (and available).

- Follow up, and maintain good communication until your loan is approved or denied.

6. How to Increase Your Chances of Approval

Here’s how to stand out:

- Provide accurate financials or projections

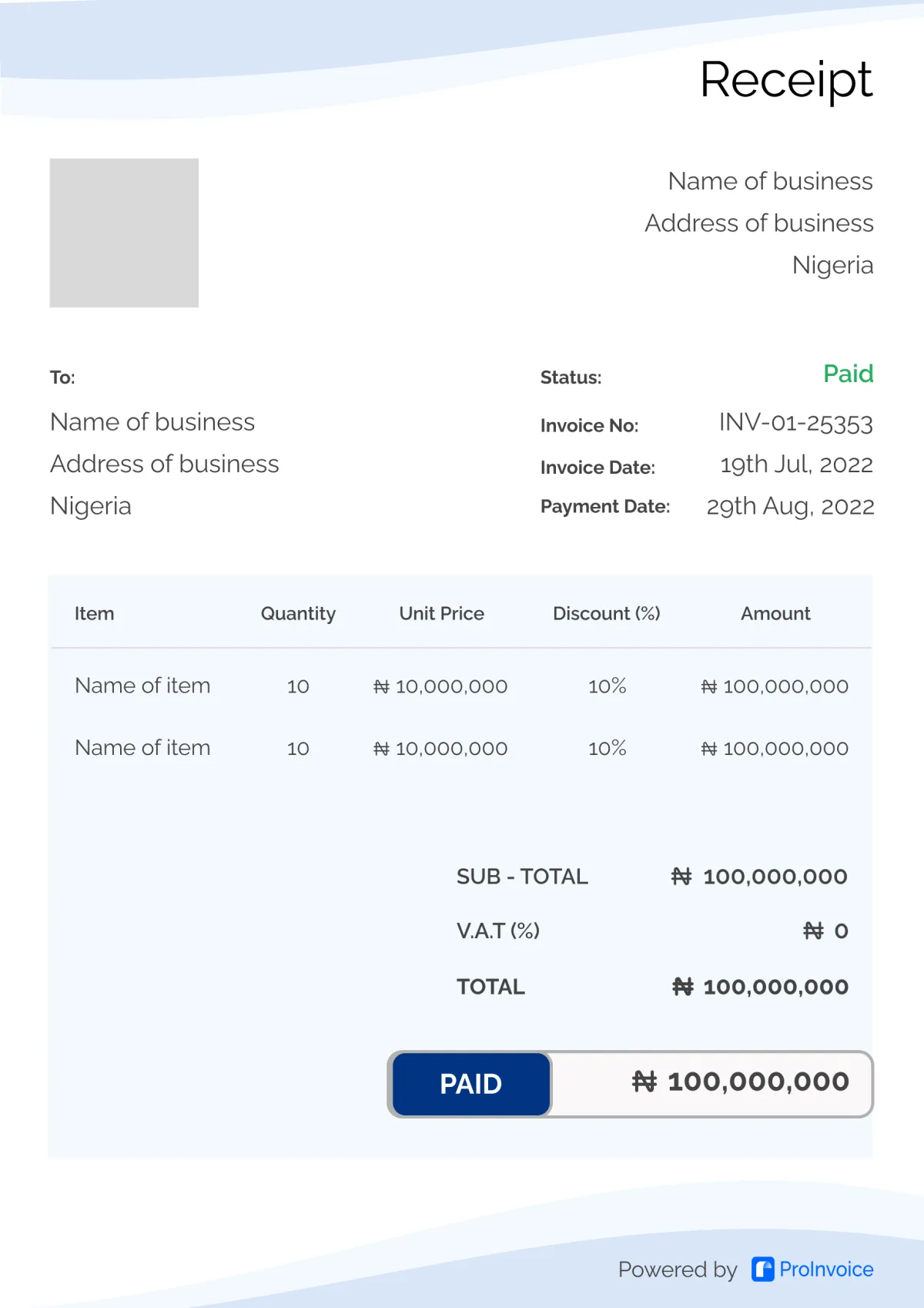

- Use brand tools to show business structure, such as ProInvoice—send sample invoices to show control and track record

- Show evidence of prior business income, even via savings or consistent payment inflows

- Offer collateral or group guarantee where needed

- Be transparent about how you will grow sales or revenue with the loan

7. What to Do After Loan Approval

Once approved:

✅ Use the funds strictly for stated business purposes

✅ Track all expenses and sales from the loan

✅ Create invoices or receipts for every transaction (especially payments to suppliers or clients) using ProInvoice

✅ Set a repayment calendar—schedule auto-transfers or manual payments

✅ Maintain good communication with lender—avoid missed payments

8. How to Track Your Loan as a Business Owner

Use tools or methods to stay organized:

- Excel or Google Sheets tracker of loan balance and repayment schedule

- Accounting app or invoicing tool like ProInvoice to record income and outflows

- Monthly review of your business sales against loan repayment timelines

Professional loan management increases trust—not only with lenders, but also with future investors or grant providers.

9. Pitfalls to Avoid When Borrowing

❌ Borrowing more than you need (leads to higher interest)

❌ Using loan funds for personal expenses

❌ Not keeping credit records or invoices

❌ Missing repayments without notice

❌ Borrowing from pyramid or unregulated schemes

If you want assistance converting payments with documentation—use ProInvoice’s free invoice tools to build good business credit early.

10. Planning for Future Growth

Smart entrepreneurs leverage one loan at a time:

- Repay the existing loan ahead of schedule if possible

- Build a track record—timely repayment, cash inflow history, documentation via tools like ProInvoice

- After successful repayment, consider applying for a bigger loan if needed

- Or explore equity funding or grants based on your business track record

Every repayment helps boost your credibility and borrowing capacity.

Key Takeaways

| Step | Action |

|---|---|

| 1 | Know how much you need and why |

| 2 | Choose a credible lending source (bank, MFI, gov’t, FinTech) |

| 3 | Prepare documents—CAC, bank statements, business plan |

| 4 | Complete application thoroughly and accurately |

| 5 | Track repayment and expenses professionally |

| 6 | Use invoicing tools like ProInvoice to document business activity |

| 7 | Plan repayment and future borrowing strategically |

Conclusion

Getting a business loan in Nigeria doesn’t have to be daunting. With the right preparation, documentation, and professionalism, you can easily qualify and grow your business.

More importantly, managing your loan as if it were a real investment—insisting on invoices, tracking all funds, and staying organized—goes a long way. Tools like ProInvoice help you establish that structure from the start.

Ready to get started? Sign up now and send your first branded invoice. It’s time to build your business with confidence and credibility.